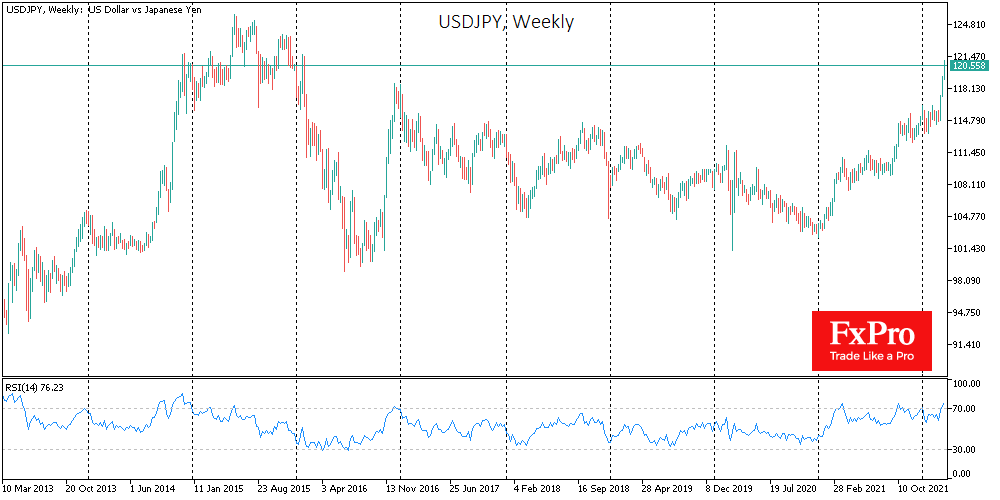

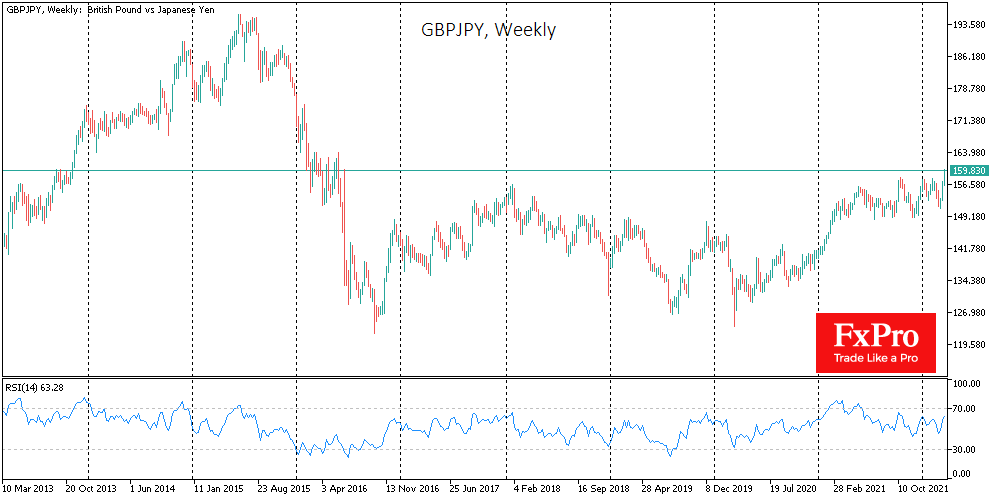

USDJPY is trading above 120.70, which was last seen six years ago, having gained more than 5% since March 7th, while GBPJPY has soared 6% and EURJPY is up 7%.

Against the yen are new comments from the Bank of Japan, which shows no sign of a change in its monetary policy, while central banks in other parts of the world issue increasingly hawkish statements.

The pressure on the yen is exacerbated by its dependence on oil and metal imports, which widens the trade deficit of the historically export-oriented country. The value of exports in February 2022 was 18% higher than in 2020, while imports soared by 49%. Booming prices for energy, metals, and agricultural products set Japan up for a further plunge into trade deficits.

In former years, sustained surpluses helped the yen maintain its strength or even strengthen during periods of market turbulence, ignoring anaemic economic growth and rising government debt to GDP levels.

The resulting crisis in commodity prices will force central banks to unambiguously choose their policy towards government bonds on the balance sheet and the general level of government debt. While the USA and Europe are tightening their rhetoric on interest rates, Japan is deliberately lagging. At the same time, the government maintains an apparent calm, pointing out that there are both disadvantages and advantages of a weak exchange rate. The yen problem is not bothering the authorities right now.

We should wait and see if investor confidence in the Japanese currency is undermined. Losing control of the exchange rate would risk an escalation of selling into Japanese government debt more than 250% of GDP. The only realistic soft solution is to deflate the national debt by accelerating inflation, but only if the central bank remains a big buyer to prevent an appreciation of the national debt. Such a policy would lead to sustained pressure on the yen.

Source: FXPro