The UAE and Saudi Arabia have significant spare capacity to restore their production to pre-demand levels and even increase their global market share. At the same time, most OPEC representatives are not fully committed to their quotas.

Iran and Venezuela have more options. Both countries are trying to use the situation to ease US sanctions pressure. Iran produces 2.3 million barrels per day, about half of pre-sanctions levels. Venezuela’s production is around 0.8m BPD versus 3.1m BPD before the 2019 sanctions. Both countries can get 0.4m b/d back on the market quickly, but it will take a significant investment in the industry and a long time to grow after that.

Caracas is already curtseying towards the US by releasing two prisoners. The US is lifting some sanctions on some Iranian politicians even before the deal is struck. These are signs of progress towards easing sanctions and a clear signal to Russia that the world is not so dependent on its energy.

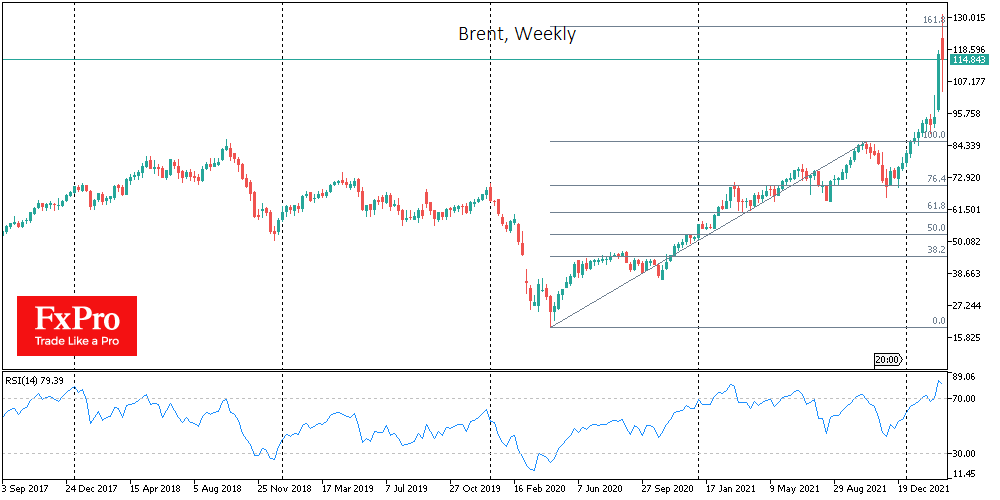

These are all signs favouring our idea that the peak of fear, and therefore oil prices, is over. Furthermore, Russia has not yet even gone so far as to threaten to halt exports as OPEC did in 1972. That said, military tensions and further restrictions on Russian oil and gas imports could trigger growth impulses, some of which could be strong. However, the oil price situation looks depleted.

We are set to see either a consolidation around these levels in a pessimistic war scenario, or a correction to around $90 on progress in the peace talks and the start of a move to ease sanctions on Russia, Iran and Venezuela.

Source: FXPro