Amongst positive factors for the US stock market are forecasts of a 50-point increase of the Federal Reserve rate at the next meeting, from the peak of 94% on the 10th of February to 33% now. But even without such extreme expectations, the market is setting itself up for the tightest monetary tightening in decades.

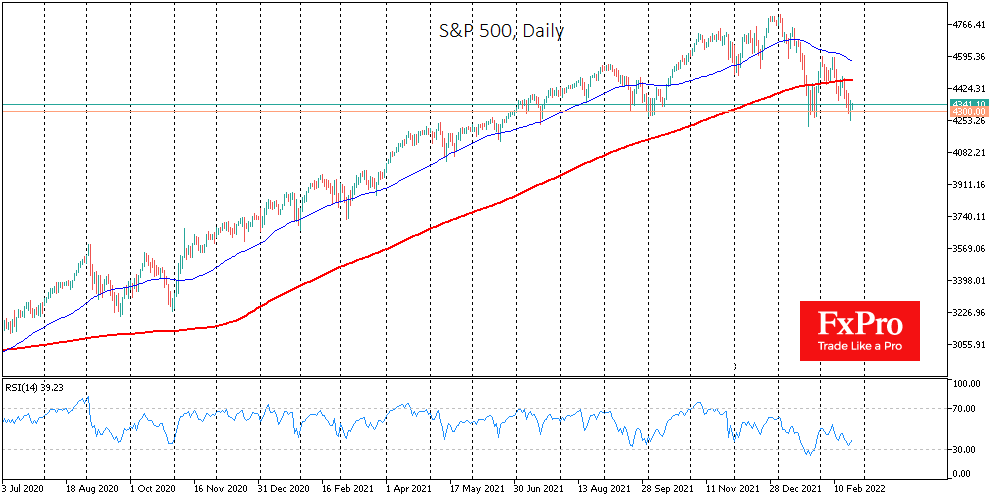

The S&P500 index formally retreated into correction territory, closing more than 10% below its peak yesterday. At the same time, as in late January, this plunge is attracting buyers to pick up cheaper securities.

Together with the pullback into correction territory, the S&P500 is once again testing the critical support area of 4250-4300.

A return to growth from this area promises to cement support and ignite momentum for continued gains, as it will show that the stock market can digest the coming tightening.

So far, however, investors should brace themselves for worse. The S&P500 lost momentum in January and recovered just a little more than half of the decline since the beginning of the month. This month, the index actively sold off when it got above the 200 SMA, generating a short-term sequence of lower local highs.

We also note that former market favourites – such as Apple, Amazon, Alphabet, Tesla – have ceased to be growth drivers. And the worse-than-expected high-tech companies – Facebook, Netflix, and some smaller, geekier ones from Roblox to Roku – are selling off almost without a bounce. Investors are punishing companies harshly for poor performance, from weak actual sales to forecasts, though they were picking them up a quarter or two ago at even weaker numbers.

And all this was happening even before the Fed started raising short-term interest rates. The “buy expectations, sell fact” model rules the markets, and so far, they are in phase one. This poised us that, at best, the pressure on equities could persist until a few days before the March meeting. A more pessimistic scenario suggests that with purchases by growth companies and the market, we will have to wait for signals from the Fed on easing rhetoric.

Source: FXPro