Jackson Hole, Wyoming, is the focal point for markets in the coming week which features little else by way of potentially earth-shaking, tier-1 data and events:

Tuesday, 23 August

- EUR: Eurozone August S&P Global PMIs, consumer confidence

- GBP: UK August S&P Global/CIPS PMIs

- USD: US August S&P Global PMIs, Minneapolis Fed President Neel Kashkari's speech

Wednesday, 24 August

- US crude: EIA oil inventory report

Thursday, 25 August

- JPY: Japan PPI

- Jackson Hole Economic Policy Symposium

- EUR: ECB minutes

- EUR: Germany GDP (final), August IFO business climate

- USD: US GDP (second estimate), initial jobless claims

Friday, 26 August

- NZD: New Zealand consumer confidence

- USD: Fed Chair Jerome Powell's speech at Jackson Hole

- USD: US July PCE deflator, personal income/spending, August University of Michigan consumer sentiment (final)

The Jackson Hole annual economic symposium, organised by the Kansas City Fed, is one of the oldest conferences where central bankers from around the world gather to discuss issues that pertain to their respective economies, and policy responses. The event has historically been seen as a platform that Fed officials use to signal upcoming policy changes.

One of the key questions for investors currently is how large future rates hikes will be, especially as we no longer have forward guidance from the Fed in an official capacity, as decisions are taken on a meeting-by-meeting basis.

Upcoming policy tightening is dependent on how strong the FOMC view the economy with a still-tight labour market and potentially falling price pressures.

As things stand, markets are forecasting a 62% chance that the Fed will proceed with a third-consecutive 75 basis point hike in September; such odds have increased dramatically from the mere 26% chance accorded at the start of August.

US equity markets have stormed higher this summer in spite of the Fed warning that a so-called “dovish pivot” from the central bank could be premature.

Will Powell push back against the market’s optimism and reconfirm its aggressive front-loaded rate hike stance, in order to get inflation back to target?

We are still over five weeks away until the next pivotal FOMC meeting, with another jobs report and inflation data still to be released. Investors will also be on the lookout for any further detail on quantitative tightening, which centres around the Fed’s reduction of its $9 trillion balance sheet. This could potentially have an impact on market liquidity so will be another important issue which could be addressed.

Interestingly, the dollar has broken higher and through several key levels ahead of the Fed’s Jackson Hole confab. Are markets already positioning for a more hawkish Powell, or is this simply summer price action with the long-term trend dominating in thin trading?

The euro is flirting with parity once more against the US dollar, through 1.01, while the British Pound is revisiting its lowest levels against the greenback since the onset of the pandemic.

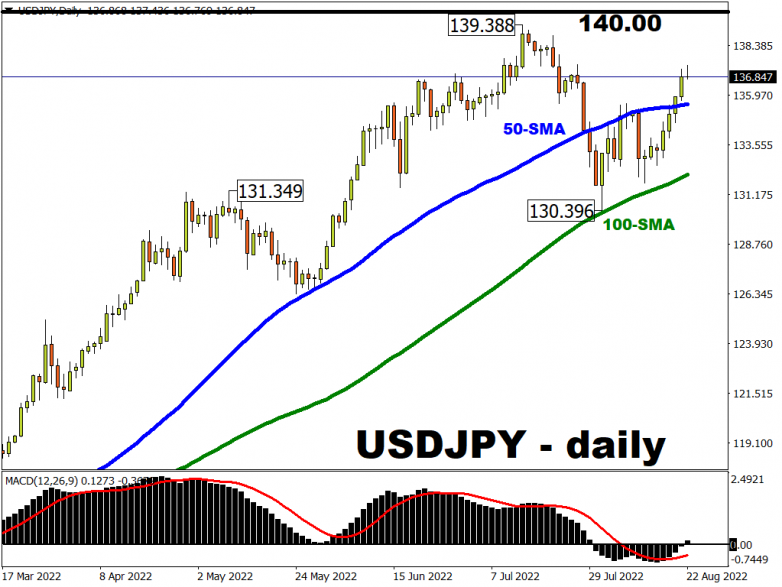

USD/JPY has resurfaced above its 50-day simple moving average and could take further strides towards the 140 mark.

These are all key levels which need to be watched if king dollar is to push on to new cycle highs, provided markets become more expectant of yet another 75bps Fed rate hike in September, depending on the Fed’s policy clues that may emanate out of Jackson Hole later this week.