It’s a very busy week of high-quality economic data which will potentially light up volatility in equity and forex markets.

Here are the scheduled economic data releases/events in the coming week:

- EUR: European Central Bank President Christine Lagarde speech

- USD: Speeches by New York Fed President John Williams, St. Louis Fed President James Bullard

Tuesday, 29 November

- JPY: Japan October unemployment, retail sales

- GBP: Bank of England’s Catherine Mann speech

- EUR: Germany November inflation, Eurozone November economic confidence

Wednesday, 30 November

- CNY: China November PMIs

- AUD: Australia October inflation

- EUR: Eurozone November inflation, Germany November unemployment

- USD: Fed Chair Jerome Powell speech, Fed Beige Book, US 3Q GDP (second estimate)

- US crude: EIA weekly oil inventory report

Thursday, 1 December

- JPY: Bank of Japan Governor Haruhiko Kuroda speech

- EUR: Eurozone October unemployment, November manufacturing PMI

- USD: US weekly initial jobless claims; October personal income/spending, PCE deflator; November manufacturing

Friday, 2 December

- USD: US November jobs report

- CAD: Canada November unemployment

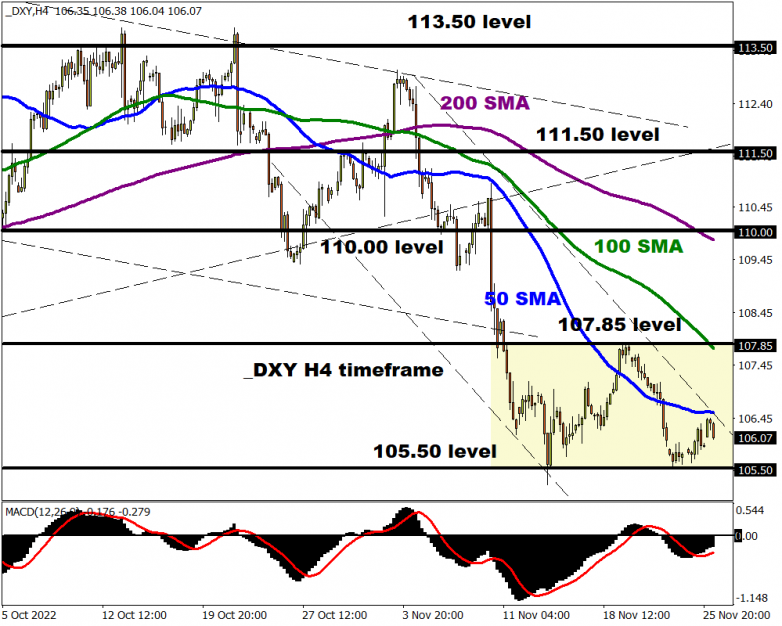

The dollar dipped lower again last week in a few holiday-abbreviated trading sessions. As we head into December, market moving risk events now pop up more frequently, beginning with inflation numbers and as always on the first Friday of the month, the US non-farm payrolls report.

We get key consumer price data on both sides of the Atlantic with the Eurozone flash estimate of HICP inflation for November and the US core PCE deflator. The Euro region data point is hugely significant as it will play a key role in the ECB’s rate decision at its meeting in a few weeks. The headline print is expected to cool slightly following the 10.6% record surge in October. With energy prices easing and other supply shocks waning, the key question is how fast this is affecting consumer prices? Money markets price in a 50bp rate hike in mid-December but this risk event is definitely one to watch. It could sway the pendulum in favour of another jumbo-sized 75bp rate increase and give a boost to the euro.

The US core PCE data is probably less followed than the timelier CPI readings, but more favoured by the Fed’s policymakers. It doesn’t always follow the path of the widely watched core CPI so certainly a 0.4% print for the core deflator could see high market volatility in the form of a dollar bounce and selloff in stocks as the Fed pivot idea is again impacted.

The end of the week brings probably the marquee event with the release of the monthly US employment report. Jobs gains should be in the region of 200,000 due to vacancies continuing to exceed the unemployed by nearly two to one. This would be the lowest reading since February last year. The jobless rate is expected to remain relatively unchanged, which should support solid wage growth at 0.3% m/m. The Fed is keen to see a steady softening of the tight labour market which will then justify a change in the pace of their policy tightening. The weekly initial jobless claims have started to rise but if there are no signs of the tightness abating, the dollar may find more willing buyers as the peak “terminal” rate would have to go above 5%.