Get ready for a rollercoaster ride across global FX markets this week!

The calendar in focus for investors and traders is packed with central bank meetings and rate decisions, a semi-annual Congress appearance from the most powerful banker in the world, and the latest US jobs report:

Monday, March 6

- AUD: Australia February inflation gauge

- EUR: Euro area January retail sales

Tuesday, March 7

- AUD: Reserve Bank of Australia decision; Australia January external trade

- CNH: China February external trade

- EUR Germany January factory orders

- USD: Fed Chair Jerome Powell testifies before Congress

Wednesday, March 8

- AUD: RBA Governor Philip Lowe speech

- EUR: Eurozone 4Q GDP (final); Germany January industrial production and retail sales; ECB President Christine Lagarde speech

- US crude: EIA crude oil inventories

- CAD: Bank of Canada rate decision

- USD: Fed Chair Jerome Powell continues testimony before Congress

Thursday, March 9

- JPY: Japan 4Q GDP (final)

- CNH: China February CPI

- USD: US weekly jobless claims; US President Joe Biden to release fiscal 2024 US budget

Friday, March 10

- JPY: Bank of Japan rate decision; Japan February PPI

- EUR: Germany February CPI (final)

- GBP: UK January GDP, industrial production, and trade balance

- CAD: Canada February jobs report

- USD: US February nonfarm payrolls report

King Dollar is ready to react to the latest Fed policy clues stemming from these key events:

-

Fed Chair Powell speaks late on Tuesday as he appears before the Senate and after the slew of bumper economic releases which have seen upside surprises across the board.

Any hints he gives as to whether he thinks the Fed should deviate from 25bp rate hikes going forward will move markets.

He could also imply that the new FOMC dot plot to be published in a few weeks will need to go higher to combat sticky core inflation.

This twice-a-year event has seen Fed Chairs in the past give views on the outlook so it will be a key focus for markets.

- The incoming US non-farm payrolls (NFP) report is the follow up to last month’s scarcely believable 517,000 job gains in January.

If an economist tells you that they know what the headline US non-farm payroll print will be, it’s fair to say that they will be guessing 100%!

After the prior blockbuster half-a-million reading, a consensus print around 200,000 is expected, but not with a lot of certainty.

Other job surveys point to a much lower figure than in January, with seasonal adjustments and weather-related issues accounting for the January blowout.

We will be on the lookout for revisions to that number and increased volatility around the jobs release.

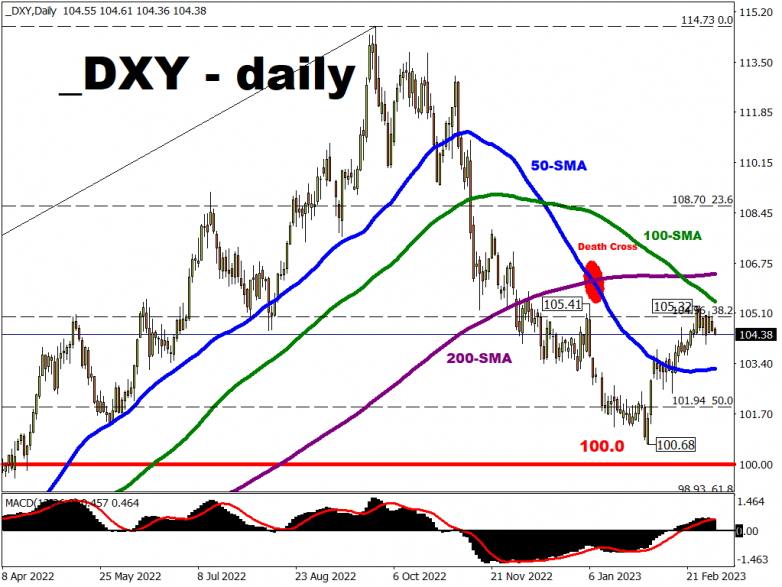

Dollar bulls will be longing for fresh cues to punch the DXY above its 100-day simple moving average (SMA).

Otherwise, either a not-so-hawkish Powell along with a lacklustre NFP report could see DXY faltering below the 104 mark and closer towards its 50-day SMA to unwind more of its February gains.

Then, moving over to the non-USD side of some G10 FX pairs, there are key central bank decisions that await:

- AUDUSD (Tuesday, March 7): The Reserve Bank of Australia is expected to continue its hiking cycle with a 25bp rate rise which will take the policy rate to 3.6%. Concerns about high inflation linger but data has surprised to the downside recently.

-

USDCAD (Wednesday, March 8): The Bank of Canada is expected to stand pat, which means leaving its rate unchanged at 4.5%.

The economy remains overheated despite the recent downside surprise in Q4 GDP, though Canada’s own jobs report due Friday should offer more recent clues on the state of this North American economy.

-

USDJPY (Friday, March 10): At what is set to be the last Bank of Japan policy meeting under the stewardship of Governor Kuroda, there is much speculation about if and when the BoJ might move away from its uber-dovish policy stance.

Yen price action will be directed by any hint at policy normalisation with the impact felt by all asset markets when that moment does come around.

While the Australian Dollar is not a constituent of the benchmark Dollar index (DXY), the Japanese Yen and the Canadian Dollar combine to form 22.7% of the DXY (13.6% for JPY, 9.1% for CAD).

Hence, how these other currencies move over the coming days should also have a notable impact on how DXY fares overall this week.