The rally in the greenback is kicking on, set for a fourth straight week of gains. Such a streak had not been seen since February.

The dollar index had closed lower for three consecutive days, but this was apparently a bullish consolidation after the strong May rebound.

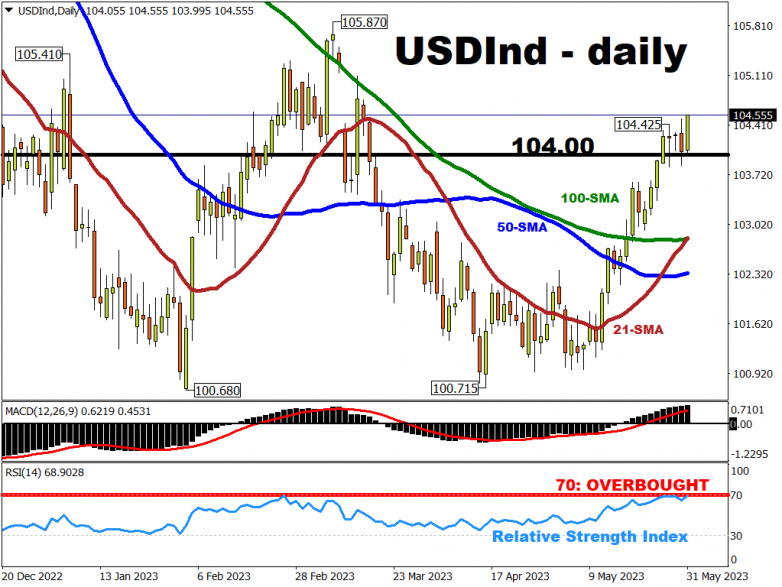

Already today’s intraday prices have set a new two-month high, with buyers hoping to push on to 105.

China’s weaker-than-expected non-manufacturing PMI, released just hours ago, have sparked a flight to safety as economic growth in the world’s second-largest economy appears to be stuttering.

Such risk-off moves have played into the hands of dollar bulls.

From a technical perspective …

Traders may draw upon on the bullish cue as the 21-day simple moving average (SMA) has now crossed above its 100-day counterpart.

However, note that this latest ascension also brings the USD Index into “overbought” territory once more, with its 14-day relative strength index (RSI) breaking above the 70 threshold.

Recall in late February, when the USD Index’s 14-day RSI flirted with overbought conditions.

Such a technical event was then followed by a 4.37% drop over the subsequent seven weeks.

A softer close in the DXY below 104 would be needed to halt the strong momentum over the past few weeks and imply a technical peak after its largely uninterrupted 2.8% climb so far this month.

From a fundamental perspective …

The ongoing fiscal drama in Washington continues to also run with hardliner Republicans voicing their disapproval at the deal.

Any confirmed resolution and signing should help risk sentiment and lift bonds to the detriment of the USD.

There’s also a contrasting view, whereby a sealed deal to life the US debt ceiling should restore faith in US assets, to the benefit of the buck.

Investors are more intently focused on what policymakers will be doing in the next few weeks for FX direction.

This may add to pressure on the USD to an extent as rate hikes are expected from the ECB and the Bank of England next month. The Bank of Japan may also join the policy tightening path as speculation mounts that it will tweak its YCC policy at its June 16 decision.

Meanwhile, the FOMC is widely expected to skip a rate hike at its June 14 meeting and reassess its policy in July, though markets currently see above a 60% chance of a 25bp hike in June.

Much of this (ECB, BoE) is priced in so guidance will need to sound hawkish to lift the EUR and GBP materially going forward, especially if either G10 currency wants to meaningfully push back against the US dollar’s resilience of late.